Minimum Coverage Requirements in Oklahoma

Oklahoma operates under an at-fault tort system, meaning the driver who caused the accident is financially responsible for damages. The state requires continuous proof of insurance — driving uninsured triggers immediate license suspension and reinstatement fees up to $250. Oklahoma mandates electronic insurance verification through the Oklahoma Insurance Verification System, allowing law enforcement real-time access to coverage status.

How Much Does Car Insurance Cost in Oklahoma?

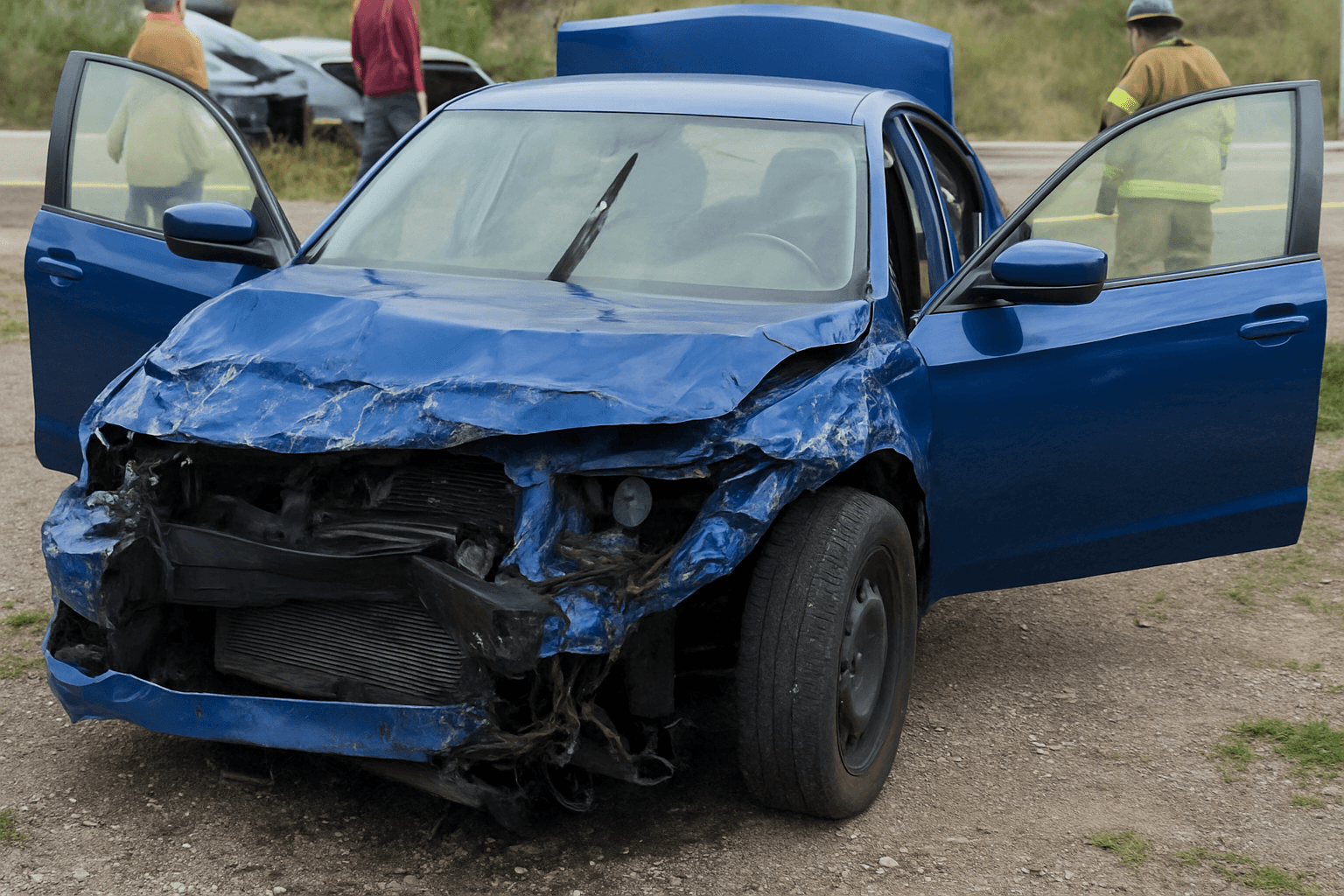

Oklahoma rates are influenced by the state's high uninsured driver percentage, frequent severe weather, and rural driving distances. Carriers price aggressively for clean-record drivers but add steep surcharges for violations — a single DUI increases premiums 80–120% for three years.

What Affects Your Rate

- Uninsured driver rate: Oklahoma's 14% uninsured driver percentage increases uninsured motorist premiums 20–30% compared to states with lower rates.

- Hail frequency: Central Oklahoma zip codes average 15–25% higher comprehensive premiums due to annual severe hail exposure.

- DUI surcharge duration: Oklahoma carriers apply DUI surcharges for 3–5 years post-conviction, adding $900–$1,800 annually.

- Rural mileage: Drivers in counties outside Oklahoma City and Tulsa metro areas often drive 40+ miles daily, increasing collision risk and raising rates 10–15%.

- Credit-based scoring: Oklahoma permits credit-based insurance scoring, allowing carriers to surcharge drivers with poor credit up to 50%.

- Age penalties: Teen drivers (16–19) in Oklahoma pay 150–200% more than adults for the same coverage due to the state's high teen accident rate.

Compare car insurance rates in your state

Get quotes from licensed carriers — no obligation, no spam, results in minutes.

Get Your Free QuoteCoverage Types

Liability Insurance

Covers injuries and property damage you cause to others. Oklahoma's at-fault system makes liability your first line of financial defense.

Uninsured Motorist Coverage

Protects you when hit by a driver with no insurance. Pays your medical bills and repairs your vehicle.

Comprehensive Coverage

Covers hail, theft, vandalism, animal strikes, and windshield damage. Non-collision events that total vehicles.

Collision Coverage

Pays to repair or replace your vehicle after an accident, regardless of who was at fault.

SR-22 Insurance

High-risk driver certification filed with the state after DUI, driving without insurance, or serious violations.

Full Coverage

Combines liability, collision, comprehensive, and uninsured motorist into one package. Required by lenders on financed vehicles.